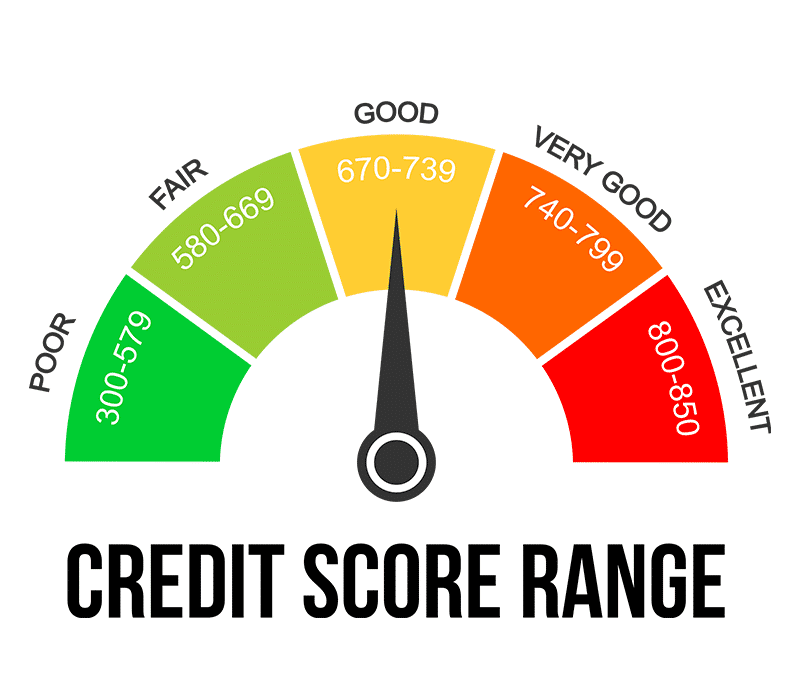

A good credit score plays a crucial role in financial stability and opportunity, especially in a growing economy like Kenya. Whether you are applying for a loan, seeking a mortgage, or even financing a business, your credit score is often the first thing lenders evaluate. It reflects your reliability in repaying debts and helps financial institutions determine your risk level.

In Kenya, credit scores are largely managed by Credit Reference Bureaus (CRBs), and a positive rating can open doors to better loan terms, lower interest rates, and quicker approvals. On the other hand, a poor credit score can limit your access to credit facilities or lead to higher borrowing costs. This makes it essential for individuals to understand and actively manage their credit profile.

Improving your credit score starts with timely repayment of loans and bills. Consistency in paying debts on or before the due date builds trust with lenders. It is also important to avoid taking multiple loans at once, as this may signal financial distress. Regularly checking your credit report from CRBs can help you identify errors or fraudulent listings that may negatively impact your score.

Another key step is maintaining a low credit utilization ratio. This means borrowing only what you need and ensuring that your outstanding debt remains manageable. Clearing existing debts and avoiding defaults will gradually improve your creditworthiness over time.

Building a strong credit score does not happen overnight, but with discipline and financial awareness, it is achievable. By managing your finances responsibly, you not only improve your credit rating but also position yourself for greater financial opportunities, security, and long-term success in Kenya’s evolving financial landscape.